The Destruction Of Nigeria's Economy

The Relevant Information No #6

If you live in Nigeria, or you have relatives/friends who live in Nigeria, you are aware that the last eighteen months have been a very economically painful time for us folks living here. From an anecdotal standpoint, the decline in economic activities has been near apocalyptic.

It’s a fairly common occurrence to see or hear of factories closing down because they cannot afford to remain in production, inter and even intra state travel has become a luxury that people can only afford if they absolutely have to pay that price.

Food and medicine are now luxuries that many people simply cannot afford, so it has become common to see families skip meals, and resort to all kinds of alternative self-help remedies when there’s an illness because they can no longer afford malaria or flu treatments.

The picture looked pretty grim over the last eighteen months, far worse than the eight years of former president, Muhammadu Buhari, but the general perception rather than 2025 might be an improvement - remember I only speak from anecdotal observations- is firmly rooted in a forecast that things are on course to get exponentially worse.

In talking to industrialists, merchants, smugglers, commercial drivers, civil servants, economists, finance guys, political operators, petroleum products dealers, soldiers etc, this is the most commonly held expectation of 2025 which I encounter.

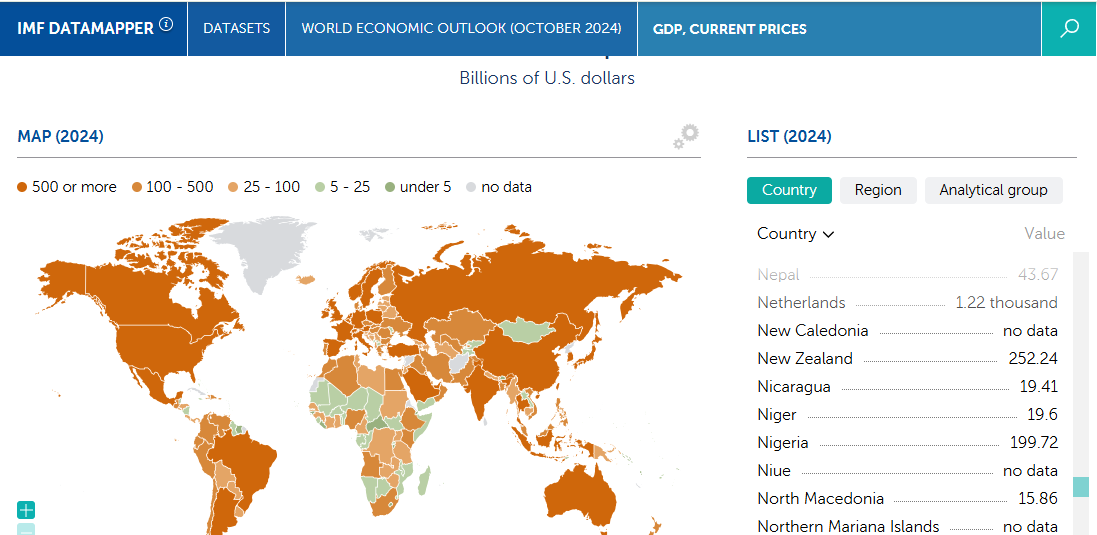

With that in mind I decided to look up on the IMF’s website, what data the world’s foremost usurer for failed/failing economies has on its site, that could help me better understand the larger picture of Nigeria’s economic outlook in this new year.

Let me say that I was not prepared for what I found.

Before I continue, let me preface by saying that I am not an economist, finance guy or in any way an expert on interpreting economic and financial data, so take my observations with the seriousness you would take the opinions of an armchair football coach.

That being said:

The first shocker for me was how badly the IMF’s data shows the Nigerian economy has completely cratered in the eighteen months that the Bola Ahmed Tinubu has been in power. In GDP nominal terms, i.e a country’s economic size/production of goods and services measured in value of US dollars. I knew it was bad, but seeing the numbers made me realise that I was not insane to perceive it as that bad.

According to the IMF, we ended the year 2024 with a GDP nominal of $199.72bn, which down from $363.82bn at the end of 2023, which means in the year 2024, the Nigerian economy shrank by $164.1bn.

This means that Nigeria’s economy basically halved within a 12 month period.

I don’t know what technical term professional economists would call this, but at my surface level understanding of numbers and how economies work, a wipeout of $164.1bn from an economy that was $363bn just a year prior, is an obliteration.

An economy that loses half its nominal productive value within one year, is very very unhealthy, nigh apocalypse levels of unhealthy.

Nigeria’s economy shrank by 164.1 billion dollars or nearly 50% in 2024 to drop to $199.72bn, from $363.82bn in 2023.

Some people - particularly partisans of the current administration - might want to argue that the depreciation of the Naira means that at current exchange rates the Nigerian economy looks smaller without actually shrinking.

However in 2016 when the Naira was wildly unstable going from roughly N200 to a dollar, up to N400 to $1 before settling at the N360/$1 it would hover around for the next six years, the IMF’s data shows that our GDP nominal dropped from the $492.44bn we ended 2015 on, to $404.65bn. Which frankly is nothing half as dramatic as the obliteration the IMF’s dataset captures in 4K resolution for 2023-2024, where we have shrunk from $363bn in the space of one year to $199bn.

If put in the context that prices for crude oil and natural gas, our two largest exports, have been high for two years running, so our economy should have been much more liquid in capital going by historical antecedents, it becomes much clearer that foreign exchange rates is not a sufficient explanation for this hollowing out of Nigeria’s economy.

For comparison, Egypt’s economy is now $380bn in GDP nominal, or nearly twice our economy’s size, this is happening in a context where FDI inflows into Egypt have severely reduced due to uncertainty over the Israeli genocide in Gaza, plus Egypt’s main source of foreign exchange - the Suez Canal - has suffered a severe drop in patronage from transiting ships due to rising insurance costs and security risks associated with the Yemeni Houthis’ campaign against ships in the Red Sea, since late 2023.

Faced with the challenges in investment and Suez Canal transit earnings caused by the Israeli genocide in Gaza, plus preexisting pressures on the Egyptian Pound, Egypt’s economy shrank by roughly $13bn from $393bn in 2023 down to the current $380bn. Nigeria with high oil and gas prices, no genocide on Gaza and similar preexisting pressure on the Naira, however completely cratered by a whopping $164.1bn in the same 12month period.

South Africa is now Africa’s largest economy at $403.05bn or twice the Nigerian economy plus give or take another $5bn in spare value change. And our we shrunk by the entire Moroccan economy plus an extra $7bn, which left us at our current position of $199bn only a tad bigger than that same Moroccan economy at $157bn or war-torn Ethiopia at $145bn.

The most striking thing for me in going through this dataset, was seeing that the IMF actually see the Nigerian economy shrinking by a further $5bn next year, and does not see it rebounding to 2023 levels in this decade at all - in fact it only sees Nigeria getting back to $268bn in 2029, about $69bn more than 2024 and almost a hundred billion dollars less than 2023.

This to me reads like the IMF is probably laughing at the funny assertions by the current administration that through its efforts we are on our way to become a $1trillion economy by 2030 and retorting with “Well actually, y’all is economically doomed for the rest of the 2020s”, a reading that in reality doesn’t seem to be off at all.

Our political elites, all of them, especially the ruling administration seem to have their heads buried up their asses when it comes to the current economic collapse and the implications it has for our immediate, mid and long term futures. Rather everybody to a T is focused now on the 2027 elections as their first, second, third, fourth, fifth and sixth priorities.

The current administration, and the National Assembly are in a manner of speaking acting with criminal negligence, if one was to go by the shenanigans contained in the N49trillion/$31.6bn 2025 Federal Government budget, that has a N13trillion/$8.4bn deficit to be funded by borrowing, in addition to a pretty heavy preexisting debt load.

Add to the situation with this vague and compartmentalised budget, the impromptu financial packages rolled out for the military’s general and flag rank officers, that the President announced recently. They are not captured in the 2025 budget but they will somehow be resourced and funded, because of their utility in keeping the general and flag rank officers of the Armed Forces happy.

When you take together, the political class’ disregard for the state of the economy, their collective focus on the 2027 elections at the expense of everything else, the multiple budgets we ran simultaneously last year, the “fantastically” engineered 2025 budget, the packages rolled out to keep the leaders of the military happy, and so on and so forth; you realise why the IMF is currently very pessimistic about Nigeria’s economic growth. And as a Nigerian, living in Nigeria, you also realise that this is a “we are not going to make it” situation, we are stuck with.

To round this up, I particularly give credence to the IMF’s data and implied analyses, because of its role as usurer (lender in polite company) to failing and failed economies, a club of which Nigeria is now a member of if you look on our streets, specifically because there’s no one that knows your economic and fiscal situation better than the person or institution that has a very vested interest in borrowing you money and making sure you pay back. For countries, that institution is to an extent the IMF.

You can download and go through the IMF’s dataset HERE

In Other News:

Last year was a particularly horrible year in Nigeria, an annus horribilis if I may, and I personally, was not left unaffected by it. The end of the year came with its own rolling bounds of challenges, one blow after the other that frankly knocked out any mental capacity in me to write out my thoughts much on anything, and maintaining this newsletter which I actually love to work on, was not something I was in the right frame to do. And I being the very terrible communicator that I naturally am, didn’t communicate that I was not in a great position to write. And for that I apologise.

I have had lots of things I wanted to opine and talk about, from the fall of the Assad regime, JNIM’s flirtation with Northern Ghana, Russia’s hard choices regarding its African operations going forward, Nigeria and Niger’s fraternal and currently combative relationship, and ISWAP. However, life has well, pretty much been “life-ing” in a not so great way, and I have just not been able to be in the space to put those thoughts down to paper so to speak.

I will try to gradually write what I can, when I can, and I am grateful that some of y’all still stick around to read my thoughts and opinions.

Seriously, thank y’all.